Introduction to GST

GST stands for Goods and Service Tax.

GST is an Indirect Tax levied on “supply” of Goods and/or Services as against the earlier concept of tax on the manufacture of goods or on sale of goods or on provision of services.

In simple words, GST can be understood as an Indirect tax applied at the time of Supply of Goods and/or Services.

It is a destination based consumption tax i.e. it is collected on Goods and/or Services by the States in which such Goods and/or Services are consumed.

History of GST

France was the first country in the world to adopt GST in the year 1954.

At present more than 160 countries have already adopted GST.

History of GST in India began on July 17, 2000 under Vajpayee Government tenure.

On September 23, 2016, GST Network was established, it is an online network designed to solve the queries of consumers and businessmen.

Assam became the first state to pass GST Act in India in August, 2016.

GST Act came into force in India from 01 July, 2017 except in the state of Jammu and Kashmir. On 07 July, 2017 State of Jammu and Kashmir also adopted GST.

Types of GST

There are 4 types of GST in India namely,

- Integrated Goods and Services Tax (IGST)

- State Goods and Services Tax (SGST)

- Central Goods and Services Tax (CGST)

- Union Territory Goods and Services Tax (UTGST)

Lets see them one by one

Integrated Goods and Services Tax (IGST)

The Integrated Goods and Services Tax (IGST) is a tax under the GST regime that is applied on the interstate (between 2 states) supply of goods and/or services as well as on imports and exports.

Under IGST, Central Government is responsible for collecting the taxes. After the collection of taxes, it is further divided by the Central Government among the respective states.

For instance, if a trader from Madhya Pradesh has sold goods to a customer in Chhattisgarh worth ₹10,000, then IGST will be applicable as the transaction is an interstate transaction.

The GST rate charged on the goods is 18%, the trader will charge ₹11,800 for the goods. The IGST collected is ₹1,800, which will be going to the Central Government.

State Goods and Services Tax (SGST)

SGST is a tax under the GST applicable on intrastate (within the same state) transactions.

In the case of the intrastate supply of goods and/or services, both SGST and CGST are charged. However, the SGST or CGST is levied by the state on the goods and/or services that are purchased or sold within the state.

It is governed by the SGST Act of that state. The revenue earned through SGST is solely claimed by the respective state government.

For example, if a trader from Chhattisgarh has sold goods to a customer in Chhattisgarh worth ₹10,000, then the GST applicable on the transaction will be partly SGST and partly CGST.

If the rate of GST charged is 18%, it will be divided equally in the form of 9% SGST and 9% CGST.

The total amount to be charged by the trader, in this case, will be ₹11,800.

Out of the revenue earned from GST under the head of SGST, i.e. ₹ 900, will go to the Chhattisgarh state government in the form of SGST.

Central Goods and Services Tax (CGST)

Just like SGST, the Central Goods and Services Tax (CGST) is a tax under GST which is applicable on intrastate (within the same state) transactions. The CGST is governed by the CGST Act.

The revenue earned from CGST is collected by the Central Government.

As mentioned in the above instance, if a trader from Chhattisgarh has sold goods to a customer in Chhattisgarh worth

₹ 10,000, then the GST applicable on the transaction will be CGST and SGST both equally.

If the rate of GST charged is 18%, it will be distributed equally in the form of 9% CGST and 9% SGST.

The total amount to be charged by the trader, in this case, will be ₹11,800.

Out of the revenue earned from GST under the head of CGST, i.e. ₹900, in the form of CGST will go to the Central Government.

Union Territory Goods and Services Tax (UTGST)

The Union Territory Goods and Services Tax (UTGST) is the counterpart of (SGST) which is charged on the supply of goods and/or services in the Union Territories (UTs) of India.

The UTGST is applicable on the supply of goods and/or services in, Daman and Diu, Dadra and Nagar Haveli, Lakshadweep, Andaman and Nicobar Islands and Chandigarh. The UTGST is governed by the UTGST Act.

The revenue earned from UTGST is collected by the Union Territory government.

In Union Territories, UTGST is a replacement for the SGST. Thus, UTGST and CGST in Union Territories will be charged together.

Features of GST

- Free flow of Input Tax Credit.

- No Cascading effect (No Tax on Tax)

- Consumption based tax.

- One Nation One Tax.

- Subsuming 17 different taxes at Central and State Level.

- Goods and Services taxed as one.

- Tax on Value addition at each stage.

- “Supply” is the taxable event.

- Comprehensive Tax.

- Dual GST is charged.

Benefits of GST

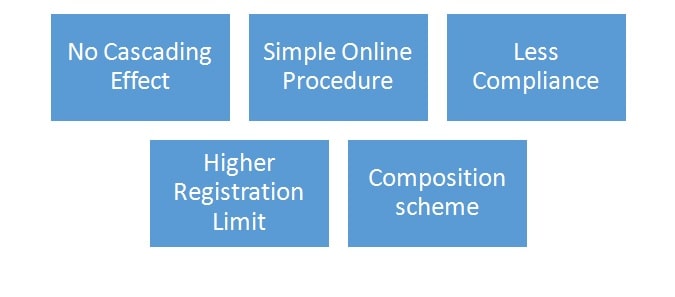

- Cascading Effect of Tax is eliminated by GST – In Simple words, In GST tax is charged on value addition at each stage, and therefore No tax on tax is charged.

- Less burden of Compliance – As opposed to the earlier tax regime, there is much less compliance under GST, Person is required to register under only one law GST as opposed to many laws like VAT, Excise, Service Tax, etc.

- Simple Online Procedure –There is only one common Portal for all compliance under GST, GST Portal provides for Registration, Return filling, Refund claims, Payment of tax, etc. at one place only. The link to GST Portal is https://www.gst.gov.in/.

- Higher Limit for Registration – Relief is provided to small businesses for registration. The Threshold limit for registration under GST is 20 lakhs (10 lakhs for NE states).

- The benefit of Composition Scheme to Small Businesses – Lower rate of tax and fewer procedures for compliance of law is provided to small businesses having turnover up to 75 Lakhs.

Taxes Subsumed By GST

Central Taxes

- Central Excise Duty;

- Duties of Excise (Medicinal and Toilet Preparations);

- Additional Duties of Excise (Goods of Special Importance);

- Additional Duties of Excise (Textiles and Textile Products);

- Additional Duties of Customs (commonly known as CVD);

- Special Additional Duty of Customs (SAD);

- Service Tax;

- Cesses and surcharges insofar as they relate to supply of goods or services.

State Taxes

- State VAT;

- Central Sales Tax;

- Purchase Tax;

- Luxury Tax;

- Entry Tax (All forms);

- Entertainment Tax (except those levied by the local bodies);

- Taxes on advertisements

- Taxes on lotteries, betting and gambling

- State cesses and surcharges insofar as they relate to supply of goods or services

Scope of GST

Important Definitions

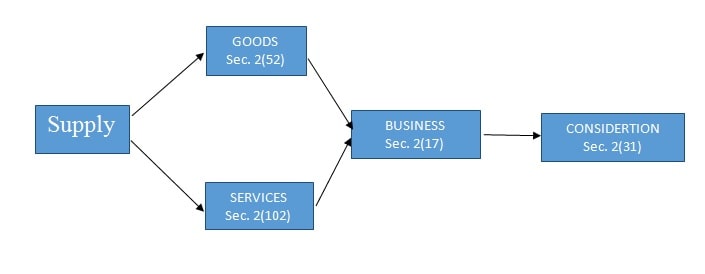

Supply

Section 7 of the CGST Act, 2017 states –

All forms of supply of goods and/or services such as

- Sale,

- Transfer,

- Barter,

- Exchange,

- License,

- Rental,

- Lease or

- Disposal.

Made or agreed to be made for a consideration by a person in course of business or furtherance of business.

Goods

Section 2(52) of the CGST Act, 2017 states –

“Goods” means every kind of movable property other than money and securities but includes actionable claim, growing crops, grass and things attached to or forming part of the land which are agreed to be severed before supply or under a contract of supply.

Services

Section 2(102) of the CGST Act, 2017 states –

“Services” means anything other than goods, money and securities but includes activities relating to the use of money or its conversion by cash or by any other mode, from one form, currency or denomination, to another form, currency or denomination for which a separate consideration is charged.

Business

Section 2(17) of the CGST Act, 2017 states –

It includes—

a. any trade, commerce, manufacture, profession, vocation, adventure, wager or any other similar activity, whether or not it is for a pecuniary benefit;

b. any activity or transaction in connection with or incidental or ancillary to sub-clause (a);

c. any activity or transaction in the nature of sub-clause (a), whether or not there is volume, frequency, continuity or regularity of such transaction;

d. supply or acquisition of goods including capital goods and services in connection with commencement or closure of business;

e. provision by a club, association, society, or any such body (for a subscription or any other consideration) of the facilities or benefits to its members;

f. admission, for a consideration, of persons to any premises;

g. services supplied by a person as the holder of an office which has been accepted by him in the course or furtherance of his trade, profession or vocation;

h. services provided by a race club by way of totalizer a license to book maker in such club; and

i. any activity or transaction undertaken by the Central Government, a State Government or any local authority in which they are engaged as public authorities;

Consideration

Section 2(31) of the CGST Act, 2017 states –

Consideration in relation to the supply of goods or services includes

(a) Any payment made or to be made, whether in money or otherwise, in respect of, in response to, or for the inducement of, the supply of goods or services, whether by the recipient or by any other person but shall not include any subsidy given by the Central Government or a State Government;

(b) The monetary value of any act or forbearance, whether or not voluntary, in respect of, in response to, or for the inducement of, the supply of goods or services, whether by the recipient or by any other person but shall not include any subsidy given by the Central Government or a State Government:

PROVIDED that a deposit, given in respect of the supply of goods or services or both shall not be considered as payment made for such supply unless the supplier applies the deposit as consideration for the said supply.

Person

Section 2(84) of the CGST Act, 2017 states –

Person includes –

- An individual;

- A Hindu Undivided Family;

- A company;

- A firm;

- A Limited Liability Partnership;

- An association of persons or a body of individuals, whether incorporated or not, in India or outside India;

- Any corporation established by or under any Central Act, State Act or Provincial Act or a Government company as defined in clause (45) of section 2 of the Companies Act, 2013;

- Any body corporatein corporated by or under the laws of a country outside India;

- A co-operative society registered under any law relating to co- operative societies;

- A local authority;

- Central Government or a State Government;

- Society as defined under the Societies Registration Act, 1860;

- Trust; and

- Every artificial juridical person, not falling within any of the above;

GST Applicability

- GST is applicable to whole of India including Jammu and Kashmir.

- GST would apply to all goods and services except Alcohol for human consumption.

- GST on five specified petroleum products (Crude, Petrol, Diesel, Aviation Turbine Fuel& Natural gas) would be applicable from a date to be recommended by the GST Council.

- Tobacco and tobacco products would be subject to GST. In addition, the Centre would continue to levy Central Excise duty.

Dual System of Taxation

Since India is a Federal State.

It would be a dual GST with the Centre and the States simultaneously levying it on a common base.

The GST to be levied by the Centre would be called Central GST (CGST) and that to be levied by the States [including Union territories with legislature] would be called State GST (SGST).

Union territories without legislature would levy Union territory GST (UTGST).

An Integrated GST (IGST) would be levied on inter-State supply (including stock transfers) of goods or services.

This would be collected by the Centre so that the credit chain remains uninterrupted.

Analysis of Above Definitions

- Goods and Service Tax as commonly referred to as GST is a Consumption-based tax charged on the Supply of Goods and Services. (GST Basics)

- GST is an Indirect Tax, thus the person on whom tax is levied and the person who ultimately bears the tax is different.

- Thus Supply is a Taxable event here. Not Manufacture/Sale of Goods or Provision of Services like in the previous tax laws (Excise, Service Tax, and Vat Laws)

- The Supply must be made in connection to the Business of the Person and must be for Consideration.

- The Supply shall be affected between persons as defined in the Act.

- Section 7 also provides for transactions that are to be treated as Supply when not made in connection to the Business or when supply is made without consideration.

- Transaction in money is neither Supply of Goods nor Service as it is out of definition and hence no GST is levied on the same. For Example, Deposit/Withdrawal of Money, Payment of Loan, etc.

- Alcohol for Human Consumption is taxed as per State Tax Laws.

- Both Excise duty and GST are chargeable on Tobacco and Tobacco-related products.

- Importation of Good and/or Service are subject to GST

- At present, five particular products are not under the scope of GST. GST to be applicable on the same from a date notified by GST Council.

- GST has replaced the old system of Taxation in India by subsuming various state and center level taxes. Thereby be called “One Nation One Tax”

- GST is collected simultaneously by the Center and state in the form of CGST, SGST, UTGST, and IGST so that there is the seamless flow of Input tax credit, unlike the old tax regime where the Center and State charge different taxes.

GST Important Links

GST Portal – https://www.gst.gov.in/

Registration – https://reg.gst.gov.in/registration/

E Way Bill – https://ewaybill.nic.in/

GST Login – https://services.gst.gov.in/services/login

GST Frequently Asked Questions (FAQs)

Goods and Service Tax as commonly referred to as GST is a Consumption based tax charged on Supply of Goods and Services.

GST stands for Goods and Service Tax.

GST Act came into force in India from 01 July, 2017.

The then Finance Minister ArunJaitley of Modi Government introduced the GST Bill in the LokSabha, where the BJP had a majority. In February 2015, Jaitley set another deadline of 1 April 2017 to implement GST. GST was finally implemented on 01 July, 2017.

Currently, there are 4 GST rate slabs — 5%, 12%, 18% and 28%.

Furtherseveral items fall in exempt category or nil duty i.e.

no tax is charged on such items. For Example, Grains like wheat, Milk etc.

GST on Petroleum products have not been notified as of date and so Excise duty and VAT are still applicable on those products. Further both GST and Excise are applicable on Tobacco and related products.

GST is charged and collected by a registered person on supply of Goods and/or Services. GST is charged on the value/selling price of the goods/services. The amount of GST incurred on purchases (input tax) can be deducted from the amount of GST charged on sales (output tax) by the registered person.

Rules framed by the Government for Various aspects of procedures related to GST such as Invoice, Returns, Composition, Valuation, and Input tax credit Rules etc. are introduced for application of the GST Law.