What is Input Tax Credit (ITC)?

In general sense, Input Tax Credit generally known as ITC refers to the tax paid while purchasing goods or taking input services, this ITC can be utilized to set off liability of tax payable on sales (Outward Supplies).

Under GST Regime, Input tax credit is available to be reduced from the output tax liability.

Let’s see an example to understand the concept of ITC

Mr. A of Rajasthan purchased certain goods from Mr. B of

Gujarat for Rs.10000/-

Being interstate purchase of Goods, he paid IGST @18% on such goods = Rs.1800/-

Total Amount paid = 10000 + 1800 = Rs.11800/-

Now, Mr. A sold the said goods to Mr. C of Madhya Pradesh after adding his profit for Rs.12000/- (10000+2000).

Being interstate sale of goods, he charged IGST @18% on the goods = Rs.2160/-

Total amount charged = 12000 + 2160 = Rs.14160/-

Now Mr. A should remit the tax collected from customer Mr. C to the government, however after deducting the tax he paid on purchase of those goods.

Total tax payable by Mr. A to government = 2160 – 1800 = Rs.360/-

This is the Concept of ITC as Mr. A gets credit of Rs.1800/- already paid by him on purchases.

And thus only value addition is taxed i.e. 2000*18% = Rs.360/-

Who can claim ITC

A person registered under the GST Law can only claim ITC, In other words, an unregistered person is not eligible to claim input tax credit of good and/or services purchased/received by him.

Thus a registered person who has purchased goods or taken any input services can claim Input tax credit (ITC) on fulfillment of certain conditions as laid down under the GST Acts and Rules to claim ITC.

Conditions to claim ITC

Following are the conditions on the fulfillment of which, a registered person can avail ITC :

- The Registered person should have received or have Possession of any of the documents such as tax invoice/debit note/other document evidencing payment of tax.

- The goods shall be delivered by supplier to a third person on the direction of a registered person against a document of transfer of title of goods

- Return should be filed.

- Receipt of goods and/or services

- Where goods are received in lots or installments, Input tax credit can be availed only on the receipt of last lot or installment

- The recipient of goods and/or services shall make payment to the supplier within 180 days from the date of supply, if not the ITC already claimed on such goods and/or services shall be reversed. However on payment made for such goods after 180 days, the recipient can again avail the ITC on such goods and/or services.

- If depreciation has been claimed on the GST component charged on the purchase of a capital good, then no ITC can be claimed.

Documents required to claim ITC

Let us understand in detail what documents are required to avail and claim Input tax credit (ITC):

- A GST invoice issued by the person from whom goods are purchased or services have been taken or both.

- In case goods are imported from outside India, Bill of Entry.

- Bill of Supply

- Invoice/Credit note issued by the Input service distributed for the distribution of input tax credit

- In cases where the value of goods and/or services or tax charged there on is less in invoice than actual goods and/or services received, the debit note issued by the supplier.

- Any other document as per GST rules which provides the evidence for payment of tax.

How ITC is availed and utilized

Under GST Law, only a registered person can avail input tax credit.

To avail ITC, one must satisfy all the conditions to claim ITC and can avail ITC by submitting GST return.

The details of input tax credit available to a registered person gets auto-populated (automatically filled) from the details/invoices uploaded by the supplier of goods and/or services to the said registered person.

In case the supplier has not filed his returns or has short filed information, the registered person cannot claim ITC to the extent the information (details/invoice) not uploaded by the supplier.

Thus a registered person should always reconcile the goods purchased with his suppliers so as to ensure properly avail his input tax credit (ITC) .

In order to understand the process of utilization of ITC, let us first understand the setoff mechanism in GST for various types of GST like IGST, CGST, SGST, UTGST and cesses etc.

- ITC of IGST : Can be utilized for payment of taxes in this order :

Output IGST > Output CGST or SGST or UTGST

- ITC of CGST : Can be utilized for payment of taxes in this order :

Output CGST > Output IGST

- ITC of SGST : Can be utilized for payment of taxes in this order :

Output SGST > Output IGST

Note: From the above, we can understand that, the input tax credit of IGST is available to be set off against first IGST and then others in any manner.

On the other hand, the ITC of CGST and SGST/UTGST cannot be set off against each other.

Further the Input Tax Credit (ITC) of any type of taxes is not available for payment of any cess or interest or late fees.

Utilization of ITC

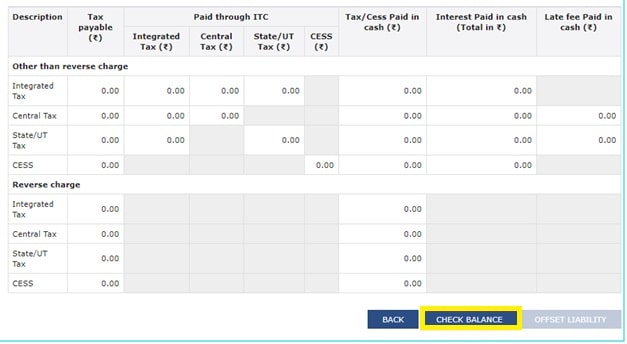

The input tax credit (ITC) available to a registered person is shown at the time of filing of return while making payment of tax.

It is on the option of the registered person to utilize the ITC in the order as they want following the GST Rules as mentioned above.

The ITC available to the registered person is shown as follows on the GST Return filing screen

Note: As you can see in the above screen, The ITC cannot be utilized for payment of output tax liability under reverse charge, the same needs to be always paid in cash.

Thus a registered person can utilize the ITC available to him for payment of output tax liability and therefore only value addition is taxed.

Time limit to avail ITC

The details of ITC is auto populated through the details/invoices uploaded by the supplier, however if there is any mismatch the same can be adjusted though returns of subsequent months.

The time limit to avail ITC from the date of invoice for which ITC is to be claimed is the September of the next year or the date on which annual return is filed whichever is earlier.

For example: Invoice date is 10 June, 20XX

Annual Return filed on 10th August of next year.

In this case the ITC pertaining to the given invoice can be claimed by 10th of August or 30th September of the following year whichever is earlier and therefore ITC can be claimed on or before 10th of August of next year only.

How to claim refund

- A registered person can claim refund of any unutilized ITC through GST Portal by applying for return. There may be various reasons due to which there can be excess credit left in ITC account or Electronic Cash ledger of a registered person for which refund can be claimed, some of them are:

- ITC for exports of goods/services without payment of tax (accumulated ITC)

- Refund for Supplies made to SEZ Unit/ SEZ Developer (With or without Payment of Tax)

- Refund of ITC Accumulated Due to Inverted Tax Structure

- Refund on Tax paid on an Intra-State Supply which is subsequently held to be Inter-State Supply and Vice Versa

- ITC for Supplier of deemed export

- Refund for excess payment of tax

- Refund on Account of Assessment/ Provisional Assessment/ Appeal/ Any Other Order etc.

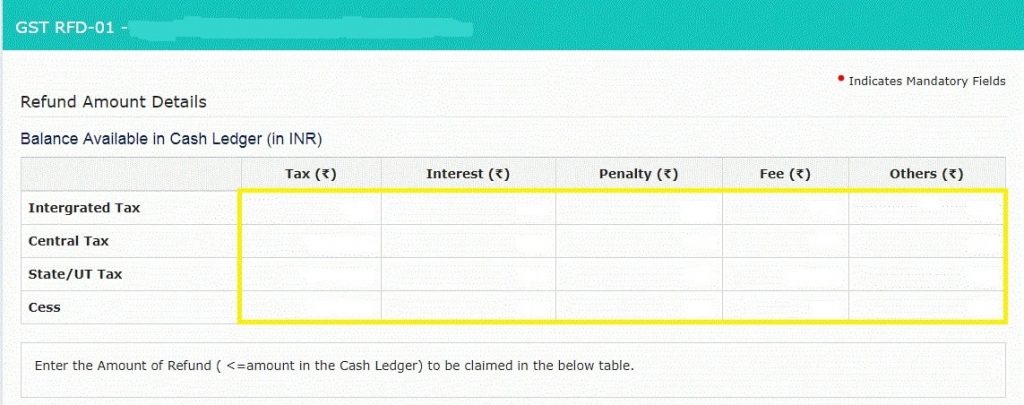

In all of the above cases, the registered person shall file GST RFD-01 to apply for refund.

GST refunds are normally processed within a month of filing the claim, However it may differ on case to case basis on the basis of processing of the return.

- Following are the steps to apply for GST Return.

- Login to GST Portal https://www.gst.gov.in/

- In Services tab go to > Refunds >Application for Refund

- Select the reason for which the refund application is to be made and click on CREATE, a new screen will appear showing details of available of excess balance for which refund can be applied.

- Here the Registered person should enter the details of ITC for which the refund is to be claimed.

- Then select the bank account in which you want your refund is to be credited from the drop down list.

- Upload the supporting document for the claim of refund.

- Select the Authorized signatory and sign the declaration by ticking the checkbox

- For final submission of the refund application form, select either of the “File with DSC” or “File with EVC” as verification option to finally submit your refund application.

- Once the GST RFD-01 is filed, an ARN will be generated, using this ARN, the registered person can keep track of the status of his refund claim.

Important Links

GST Portal – https://www.gst.gov.in/

GST Login – https://services.gst.gov.in/services/login

Portal Refund Help – https://www.gst.gov.in/help/refund

GST Refund – https://services.gst.gov.in/services/quicklinks/refunds

Track Application Status – https://refund.gst.gov.in/refunds/pre/trackarnstatus

Frequently Asked Questions (FAQs)

Input Tax Credit generally known as ITC refers to

the tax paid while purchasing goods or taking input services, this ITC

can be utilized to set off liability of tax payable on sales (Outward

Supplies). Under GST Regime, Input tax credit is available to be

reduced from the output tax liability.

Under GST Law, GST Rules have been formulated to provide with proper understanding of the ACT and to subordinate the GST Act by providing procedural and other information for the people. GST Rules for ITC are in place and deal with, manner of utilization of ITC, Blocked credits, how to file returns and which forms are required etc. GST Rules are supplementary to the GST Act.

To check the balance of ITC available one can login to the GST portal and select the latest filed return from the services tab using the return options and check balance of ITC available there.

Under GST, the term Goods includes Capital Goods and therefore full ITC is available for the amount of tax paid on purchase of Capital Goods. However if depreciation is being claimed on the tax component of the amount of purchase, then ITC cannot be claimed for such capital goods.

Under the GST Law, ITC is available to the Principal who has sent goods to job worker for processing for tax paid on such goods. However there is a time limit within which the Job worker shall return the processed goods to the principal. The time limit is:

For Input goods – 1 year from effective date and 3 years for capital goods.

If the job worker hasn’t returned the goods to the principal before this time limit, The ITC availed on such goods shall be reversed.

Under RCM, the GST Liability is to be discharged in cash. The tax paid under RCM can be availed as ITC and utilized for payment of Output tax liability.

No, only a registered person can claim ITC of Goods and/or services taken in the course or furtherance of business. Thus GST input tax credit is not available for personal expenses.

The registered person can claim input tax credit only on the receipt of the last lot or installment.

A registered person can claim ITC for any goods and/or services on or before the earlier of last day of the September month of the subsequent year or the date of filing of annual return.

Motor vehicles falls in the category of goods on which ITC is blocked. Hence no ITC is available on purchase of motor vehicles (as capital goods) even if purchased for business purpose.

No a composite dealer cannot claim ITC. The tax paid on purchase of goods and/or services by the composite dealer shall form part of the expenses of purchase.

No, the ITC of CGST cannot be used to set off the output liability of SGST and vice versa. Cross utilization is not possible under GST.

No, ITC cannot be utilized for payment of any Cess, Interest, Late fees or penalty. The ITC can only be used for payment of tax component and can be utilized in the manner set out as per the GST Law.